Portugal Debt Crisis

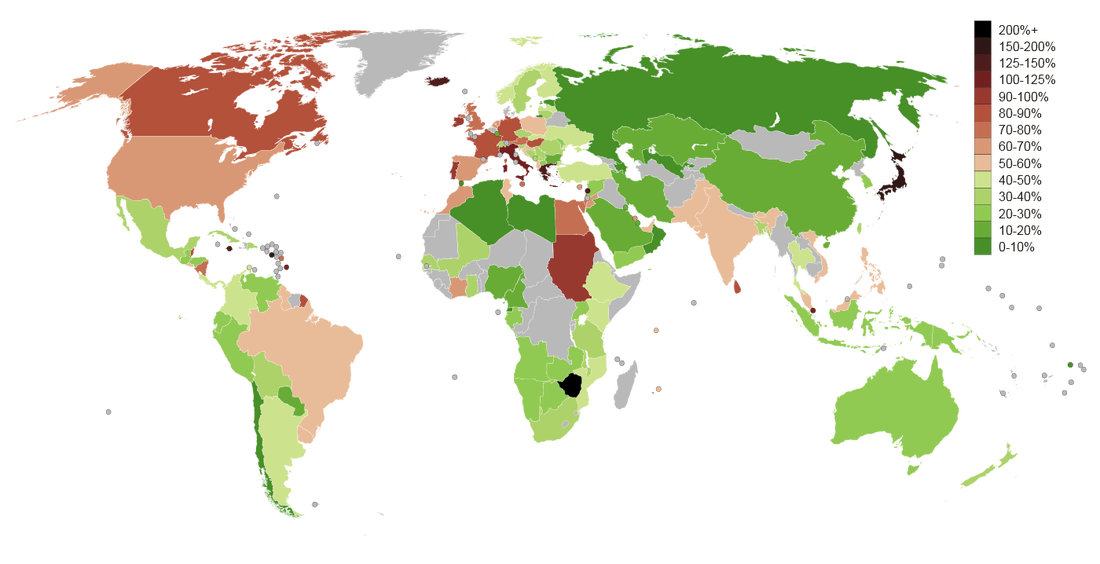

Public debt as a percent of GDP (2010)

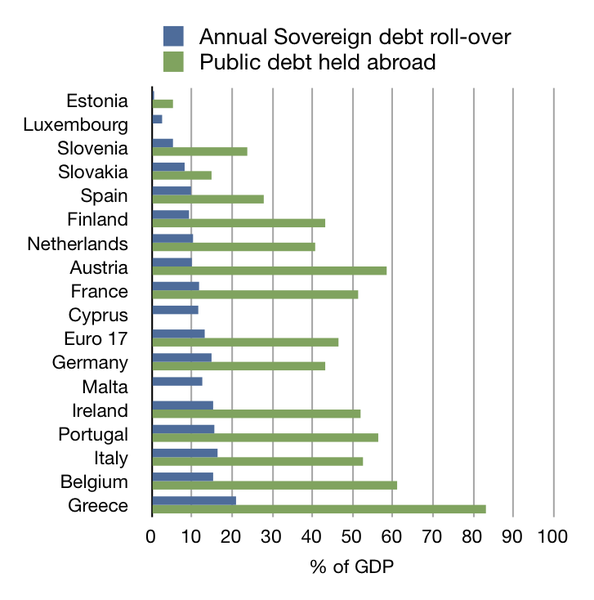

European Dept Crisis

The European sovereign debt crisis resulted from a combination of complex factors, including the globalization of finance; easy credit conditions during the 2002–2008 period that encouraged high-risk lending and borrowing practices; the 2007-2012 global financial crisis; international trade imbalances; real-estate bubbles that have since burst; the 2008-2012 global recession; fiscal policy choices related to government revenues and expenses; and approaches used by nations to bail out troubled banking industries and private bondholders, assuming private debt burdens or socializing losses.

GDP growth in 2006, at 1.3%, was the lowest in all of Europe. In the first decade of the 21st century, the Czech Republic, Greece, Malta, Slovakia, and Slovenia all overtook Portugal in terms of GDP (PPP) per head. Greece had been a regular comparison point for Portugal since EU adhesion as both countries were formerly ruled by authoritarian governments and share similar EU-membership history, number of inhabitants, market size and tastes, national economies, Mediterranean culture, sunny weather, and tourist appeal; however, the Greek economic and financial wealth of the first five years of the 21st century was artificially boosted and was hampered by lack of sustainability, and they were caught out by a massive crisis by 2010. Portuguese GDP per head has fallen from just over 80% of the EU 25 average in 1999 to just over 70% in 2007. This poor performance of the Portuguese economy was explored in April 2007 by The Economist, which described Portugal as "a new sick man of Europe". From 2002 to 2007, the unemployment rate increased by 65%; the number of unemployed citizens grew from 270,500 in 2002 to 448,600 in 2007. By December 2009, the unemployment rate had passed the 10% mark.

Additionally, the number of government employees rose sharply despite a stable rate of population. 1979 372,086 1983 435,795 1986 464,321 1988 485,368 1991 509,732 1996 639,044 1999 716,418 2005 747,880 In 2008 and 2009 two banks, Banco Português de Negócios (BPN) and Banco Privado Português (BPP) had large losses due to bad investments, embezzlement and accounting fraud. To avoid financial crisis, the government bailed them out. However, by April 2011 the government itself would need its own bailout as it was declared insolvent. In the first half of 2011, Portugal requested a €78 billion IMF-EU bailout package in a bid to stabilize its public finances. These measures were put in place as a direct result of decades-long governmental overspending and an over bureaucratized civil service. After the bailout was announced, the Portuguese government headed by Pedro Passos Coelho managed to implement measures to improve the State's financial situation and the country started to be seen as moving on the right track. However, this also lead to a strong increase of the unemployment rate to over 15 percent in the second quarter 2012 and it is expected to rise even further in the near future. Portugal’s debt was in September 2012 forecast by the Troika to peak at around 124% of GDP in 2014, followed by a firm downward trajectory after 2014. Previously the Troika had predicted it would peak at 118.5% of GDP in 2013, so the developments proved to be a bit worse than first anticipated, but the situation was described as fully sustainable and progressing well. As a result from the slightly worse economic circumstances, the country has been given one more year to reduce the budget deficit to a level below 3% of GDP, moving the target year from 2013 to 2014. The budget deficit for 2012 has been forecast to end at 5%. The recession in the economy is now also projected to last until 2013, with GDP declining 3% in 2012 and 1% in 2013; followed by a return to positive real growth in 2014. Portugal Bailout

The tripartite committee led by the European Commission with the European Central Bank and the International Monetary Fund, that organized loans to the governments of Greece, Ireland and Portugal. Portugal received €26 billion from each member.

The government and the IMF predict an economic contraction of 1 percent in 2013 for a third straight year of recession. The jobless rate, currently at a record 15.9 percent, is seen climbing to 16.4 percent.

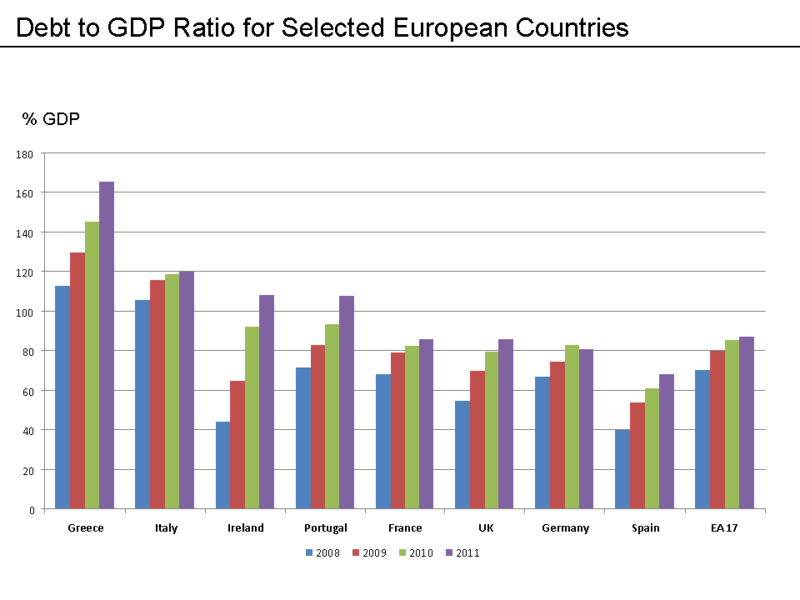

An ensuing drop in tax revenue has compelled the coalition government to step up austerity measures to shore up its finances, including what the finance minister calls an "enormous" increase in income taxes next year that will cost many workers the equivalent of a month's pay. That has brought a broad outcry from opposition political parties and from trade unions, who have called a general strike next month. Recent demonstrations have drawn tens of thousands of people, though Portugal has not so far witnessed the street violence seen in Greece. Portugal Public debt: 112.8% of GDP (2011 est.) country comparison to the world: 11 93.3% of GDP (2010 est.) note:data cover general government debt, and includes debt instruments issued (or owned) by government entities other than the treasury; the data include treasury debt held by foreign entities; the data include debt issued by subnational entities, as well as intra-governmental debt; intra-governmental debt consists of treasury borrowings from surpluses in the social funds, such as for retirement, medical care, and unemployment; debt instruments for the social funds are not sold at public auctions 2 Japan 211.70 2011 est. 4 Greece 161.70 2011 est. 11 Portugal 112.80 2011 est. 12 Ireland 105.40 2011 est. 35 United States 67.70 2011 est. 132 Chile 9.20 2011 est. Recent Events

Portugal managed to raise €1.85 billion ($2.4 billion) in a debt auction October 17th despite the country's bleak economic prospects and growing political tension over austerity policies.

The Public Debt Agency said it sold 3-, 6- and 12-month Treasury bills, with interest rates on the shortest and longest bills sharply lower though the 6-month rate was up on the last auction. The debt crisis and austerity measures have fueled the country's worst recession since the 1970s, undermining tax revenues. The government said it would work on spending cuts in addition to those already budgeted for in 2013. Next year's budget deficit goal of 4.5 percent of gross domestic product equals a gap of around 7.5 billion euros. The International Monetary Fund warned earlier this month of growing risks to the deficit-reduction program due to lower tax revenues, growing popular resistance to austerity and the likelihood that the country will remain in recession next year. Portugal's ruling coalition parties said on Monday, October 29th that they will not run against each other in next year's local elections, sending a signal of unity before Wednesday's vote on a tax-heavy draft 2013 budget aimed at meeting the country's bailout goals. The 2013 budget bill was passed by the ruling coalition with decent by the Socialists during the parliamentary session on October 31st. It imposes sweeping tax hikes. Due to the cost high cost it is expected to be challenged in the courts. |

Demonstrators protest austerity measures in Lisbon on Oct. 24, 2012

|